Let’s be honest: it’s fun to root for the bad guy sometimes. From sophisticated crews planning intricate heists to bank-robbing couples on a cross-country spree, some of our greatest tales center on criminals.

At least one film (2002’s Catch Me if You Can) focused on a famed check forger, Frank Abagnale. But how many movies have been made about his counterpart, the humble Deposit Operations Specialist? Criminals make fine folk heroes and Hollywood characters, but in the real world, real people suffer.

In 2025 alone, 76% of organizations reported instances of check fraud. And to be clear, it’s far from the romantic, Robin Hood-inspired caper of the silver screen. These are not bad actors with honorable motives – just thieves.

Now, with easy access to powerful AI tools, criminals are devising new ways to gain access, steal funds, and wreak havoc of a kind that Frank Abagnale could scarcely imagine. New check fraud detection software is needed to address a growing trend scaling at the same breakneck pace as artificial intelligence itself.

The State of AI Fraud Detection for Banks & Credit Unions

It’s a common misconception that criminals are always one step ahead of the good guys. New scams seem novel when they happen to everyday people, but chances are good that somebody somewhere saw it coming and was already working on a way to stop it.

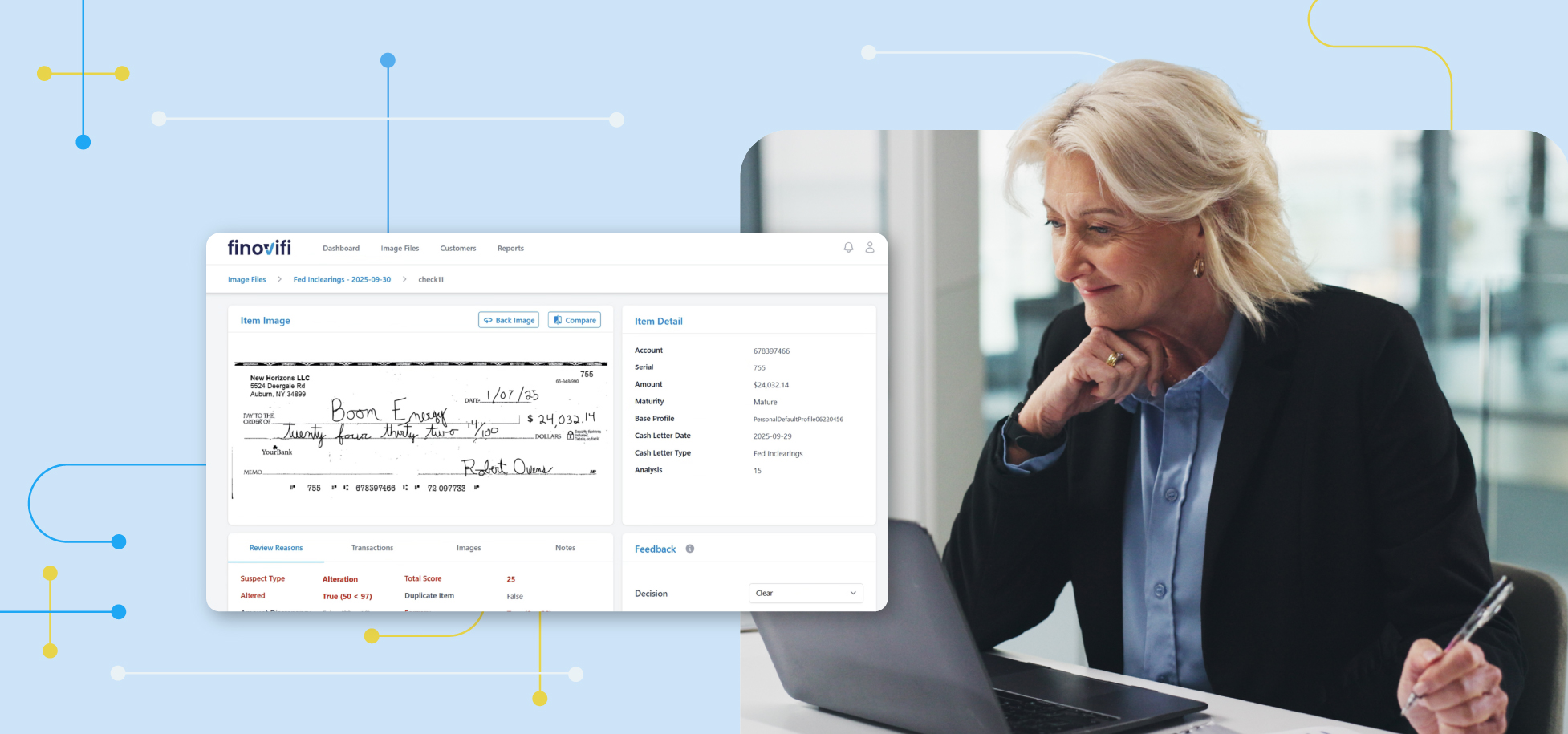

To explain how check fraud detection works, we’ll be looking at Finovifi by Main Street – the technology behind it, the methods it uses, and how it combines several forms of analysis to arrive at a single risk score.

How 21st Century Check Fraud Detection Actually Works

Funnily enough, AI-powered software depends on a much older form of technology – photography. Every check deposited at a financial institution is run through a check scanner, providing the raw data necessary for in-depth analysis.

But that image isn’t simply reviewed at a glance. Modern detection software evaluates each item across multiple dimensions, looking for inconsistencies that would be difficult – or impossible – to catch through manual review alone.

Here’s how Finovifi by Main Street determines risk, check by check.

Image Analysis

The first layer of review starts with the check itself. Image analysis looks at the physical characteristics captured in the scan – signature, layout, spacing, and the relationship between written and numerical amounts.

Subtle inconsistencies in these elements can point to alteration or forgery, even when the check appears normal at a glance.

Transactional Analysis

From there, the check is evaluated in context. Transactional analysis compares the item against expected patterns, flagging things like unusual amounts, out-of-sequence check numbers, or activity tied to new or previously monitored accounts.

What might seem like a routine deposit in isolation can stand out when viewed alongside prior behavior.

Operational Review

Certain issues are less about intent and more about execution. Operational review accounts for missing or mismatched details like dual signatures that don’t align, poor image quality, or inconsistencies in how the check is completed.

These signals don’t always indicate fraud on their own, but they contribute to a broader picture of risk.

Account Review

Finally, the system considers the account itself. Is it active and in good standing? Does the transaction align with typical behavior for that account? By comparing the check against historical activity, account review helps identify deviations that might otherwise go unnoticed in a manual process.

Combining Four Types of Analysis to Determine Risk

Each of these layers contributes a piece of the picture. On their own, they may not be enough to confirm fraud – but taken together, they form a more complete view.

Finovifi by Main Street brings these signals together into a single, consolidated assessment. Instead of relying on one indicator, the system weighs multiple factors at once, producing a score that reflects how likely a check is to be fraudulent.

This approach doesn’t eliminate uncertainty, but it does create consistency. Every check is evaluated using the same criteria, and every potential issue is measured against the same standard before it reaches a human reviewer.

From Analysis to Action: What Happens Next

Once the multi-analysis score is established, the process shifts from analysis to decision-making.

Rather than reviewing every check that passes through the system, staff are presented with a focused report of items that exceed a defined risk threshold. These are the checks that warrant closer attention.

For most institutions, that review happens at the start of the day. Checks deposited through the branch, ATM, or mobile channels – during business hours or after – are analyzed continuously, then surfaced in a single report for manual review.

From there, the workflow is straightforward. Each flagged item is reviewed in context, using both the supporting data and the institution’s own risk posture to determine whether it should be accepted or escalated.

The difference is not in the decision itself, but in how that decision is reached. Instead of working through a broad queue of checks one by one, staff can focus on a smaller subset of items that have already been identified as higher risk.

What Types of Check Fraud Can Detection Software Catch?

The patterns identified through image, transactional, operational, and account analysis map directly to the most common forms of check fraud. While no system can prevent every loss, modern detection tools are designed to surface the kinds of activity institutions encounter most often, including:

Why Check Fraud Detection Is Changing

For years, detecting check fraud depended on time, experience, and attention to detail. But as volumes increase and fraud tactics evolve, that model becomes unsustainable.

Manual review isn’t inherently flawed – but it is limited. It depends on what can be reviewed in a given window and what can be identified in the moment. As fraud becomes more subtle and more frequent, those constraints become more apparent.

Modern detection systems take a different approach. By applying the same level of analysis to every check and surfacing the items that warrant attention, they introduce consistency into a process that has traditionally varied from one review to the next.

The goal isn’t to replace human judgment. It’s to make that judgment more focused so that time and attention are spent where they have the greatest impact.

See How AI-Powered Check Fraud Detection is Only Getting Stronger

Nobody’s lining up to watch a major Hollywood production about AI check fraud detection. But here in the real world, software like Finovifi by Main Street and the people who use it are the actual heroes.

The cost of check fraud goes well beyond the dollar amount on the check itself. Staff time is diverted from everyday operations, internal processes slow down, and account holders are left dealing with the fallout.

Over time, repeated incidents can erode trust and introduce additional oversight, increasing both the operational and reputational burden on financial institutions. For those reasons (among many others), it’s time to choose a tool that stays one step ahead.

Find Out What Finovifi by Main Street Can Do at Your Institution

After 25 years of service, Main Street knows what community financial institutions need to defend, grow, and thrive. Finovifi by Main Street represents a new defense against emerging threats powered by emerging technologies. Learn more about our AI-powered check fraud detection software and get the protection your institution deserves.

Sources:

Association for Financial Professionals. 2025 AFP Payments Fraud and Control Survey Report. Accessed April 24, 2026. https://www.financialprofessionals.org/training-resources/resources/survey-research-economic-data/details/payments-fraud.

Butler, Rabihah. “AI-Powered Fraud: 5 Trends to Watch.” Thomson Reuters, accessed April 24, 2026. https://www.thomsonreuters.com/en-us/posts/corporates/ai-powered-fraud-5-trends/.